Later this week the board of the California State Teachers Retirement System, or CalSTRS, will forward to the Legislature a report laying out options for raising higher contributions into the pension system to ensure its long-term viability.

The Legislature has avoided action for a decade, and Gov. Jerry Brown’s budget forecast for education, with healthy projections for revenue, doesn’t take into account the daunting cost of teachers’ pensions on the expense side of the ledger.

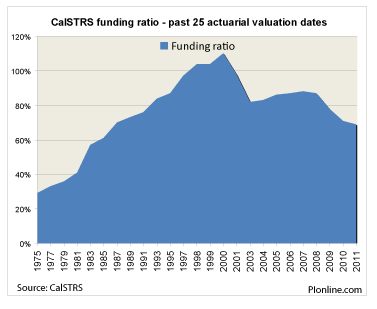

Funding ratio of CalSTRS’ defined benefit program for the past 35 years, through 2011. After being fully funded by 2000, the Legislature expanded benefits. Values fell, recovered, then plummeted in 2008. (Click for a clearer image)

The remedies won’t come cheap. The choice that CalSTRS financial analysts recommend would boost payments, currently about $6 billion, by $4.5 billion per year, starting next year. That amount, a whopping 75 percent increase per year – would be borne mostly by the state and by K-12 and community college districts, as employers and not by current employees. If adopted by the Legislature, that option – diverting billions of dollars from the classroom into pensions – could dampen, if not dash, districts’ hopes for replenishing their own depleted budgets. Yet that option, which CalSTRS CEO Jack Ehnes is expected to recommend in a cover letter to the report, is the only one that would restore CalSTRS’ defined benefit program to full funding in 30 years, consistent with federal government accounting standards.

Anticipating that lawmakers would want to dodge that bullet, however, the 26-page report presents seven other, cheaper alternatives that would fall well short of that 30-year, 100 percent funding goal – by delaying the start of higher contributions by a few years, phasing in increases gradually or aiming for only 80 percent funding. Setting a target of 80 percent of funding over 30 years would lower the contribution increases from 15.1 percent to 12.1 percent, requiring $3.6 billion in annual increases, about $1 billion less, split among districts and the state.

Another option is to stretch out the goal of full funding to 75 years. But even that target would still cost $2.9 billion more in yearly payments into the pension system while leaving CalSTRS only 62 percent funded after 30 years. That option also would saddle additional generations of state taxpayers and teachers with decades more of higher payments.

One alternative not presented is to do nothing. CalSTRS would then gradually deplete its assets and go broke in 2046. At that point, it would convert to a pay-as-you-go pension system, requiring contributions equaling 50 percent of an employee’s pay, according to the report.

Next to CalPERS, which serves other state and local public employees, CalSTRS is the state’s second largest pension system. It’s still recovering from the 2008 plunge in real estate values and the stock market slide that wiped out 25 percent of the value of the portfolio for CalSTRS’ defined benefit program and has left it only 69 percent funded to meet its long-term obligations; liabilities to current and future retirees exceeded assets by $64 billion.

That was as of June 30, 2011, the most recent year that the CalSTRS board has to act on. Reflecting recent gains in the stock market, however, CalSTRS had an impressive 13.5 percent rate of return for the year ending Dec. 31, 2012. The value of its assets – $157.8 billion on Dec. 31 – edged closer to its high point of $172 billion in 2007.

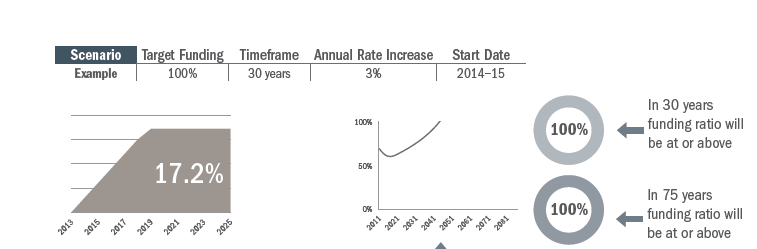

Two different options for CalSTRS’ recovery. Under this scenario, the $64 billion deficit would be wiped out in 30 years by raising contributions, as a percentage of an employee’s pay, 17.2 percentage points, by increments of 3 percent annually, starting next year. The value of assets would actually continue to fall for the first few years, then steadily rise. Source: CalSTRS. (Click for a clearer image)

However, recent gains don’t make up for years of lost earnings. Had the target annual return on assets of 7.5 percent been met since 2000, CalSTRS would be more than fully funded. Instead, the report notes, it would now take five straight years with a 17 percent return on assets, followed by 25 years of hitting the earnings goal of 7.5 percent annually, to reach full funding without the need for additional payments into the system – an implausible scenario. Last year, at Brown’s urging, the Legislature passed a package of public employee pension reforms. But because reduced pension benefits will affect only employees hired after Jan. 1, 2013, nearly all of the savings to the system won’t be felt for decades, and won’t reduce the need to deal now with CalSTRS’ deficit.

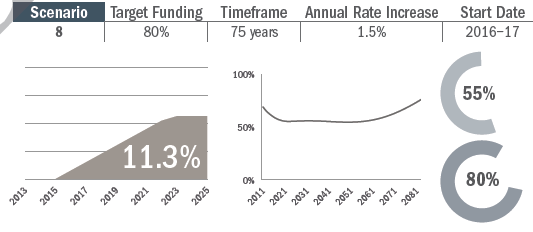

Under this option, which CalSTRS actuaries would discourage the Legislature from adopting, the goal would be only 80 percent fully funding the pension program in 75 years, not 100 percent funding in 30 years, by adding incremental contributions of only 1.5 percent of an employee’s pay per year, leveling out at 11.3 percent more. But at the end of 30 years, the program would be only 55 percent funded, leaving it more vulnerable to stock market swings. Source: CalSTRS (Click for a clearer image).

CalSTRS has relied on gains in investments to meet 58 percent of the obligations paid out to retirees and on contributions from teachers, K-12 and community college districts and the state for the other 42 percent. Unlike the CalPERS board, which can adjust the amount that government employers have to pay into the system – and already has ratcheted rates upward – CalSTRS must rely on the Legislature to set contribution levels.

Payments into the system currently total 21.45 percent of a teacher’s or administrator’s pay, split three ways.

- The employee pays 8 percent (a level that’s been constant since 1972);

- The district as employer pays 8.25 percent;

- The state pays 5.2 percent.

To reach full funding in 30 years would require additional contributions of 15.1 percent of pay by some combination of the employee, the school district and the state, bringing in $4.5 billion to the system, as of July 1, 2014. But here’s the rub: The Legislature could make new school employees share the increase, but courts have ruled that the Legislature can’t increase the contribution rates of current school employees without giving them a benefit equal to the value of their increased contribution, like higher pay. The result: The state, through the General Fund, and districts will have to absorb most of any increase in contribution levels. The report suggests that there may be a way, by deft legal maneuvering, to increase employee contributions by a maximum 2.6 percentage points.

One important, unresolved question is whether higher CalSTRS contributions by districts would require the Legislature to increase Proposition 98 funding for K-12 and community colleges by an equal amount. A 2006 opinion by the Attorney General’s office said no; the Legislative Counsel disagreed, according to the report. Without an increase in Proposition 98 funding, districts would have to absorb higher pension costs within their existing budgets. Each percentage point increase in contributions would cost the General Fund or districts about $300 million, according to the report.

There is no easy solution

During their discussion of the report last Friday, some board members expressed reluctance to even offer options that clearly would not get CalSTRS to full funding, like the 75 year payback period or raising contributions less than a percentage point per year or just enough to push back insolvency a few years.

“It is human nature; legislators will look for the cheapest way out,” said California’s Chief Deputy Superintendent Richard Zeiger. “We need to say that some of the options will not meet the fundamental requirement.”

Regardless of what the Legislature does now, it will have to adjust CalSTRS’ contributions periodically, because there will be years when the system exceeds its projected rate of return, and years, like 2008, when it falls drastically short.

To get more reports like this one, click here to sign up for EdSource’s no-cost daily email on latest developments in education.

Comments (15)

Comments Policy

We welcome your comments. All comments are moderated for civility, relevance and other considerations. Click here for EdSource's Comments Policy.

Paul 11 years ago11 years ago

Pages 9 and 10 of the draft report contain this interesting observation: "One idea that has been suggested to reduce DB Program liabilities for future members is to require they participate in Social Security for their public education service, and reduce the benefits paid under the DB Program. ... "[T]he cost of providing benefits to California public educators exclusively through the DB Program is less than it would cost to provide those same benefits from a combination of … Read More

Pages 9 and 10 of the draft report contain this interesting observation:

“One idea that has been suggested to reduce DB Program liabilities for future members is to require they participate in Social Security for their public education service, and reduce the benefits paid under the DB Program.

…

“[T]he cost of providing benefits to California public educators exclusively through the DB Program is less than it would cost to provide those same benefits from a combination of a reduced DB Program and Social Security. This is primarily because CalSTRS reduces its program costs by pre-funding its benefits, that is, investing contributions received while the member is working, an attribute that does not exist in Social Security.”

Paul 11 years ago11 years ago

There is no notion of "vesting" in Social Security. Vesting means gaining an irrevocable and individual right. Social Security participants become eligible for disability and retirement benefits after they accumulate enough quarters of covered employment, but these benefits never really belong to the individuals in question; the benefits can be changed at any time, by legislation. Worse yet, while pension plans like STRS are at least nominally funded (money is accumulated to offset the cost of … Read More

There is no notion of “vesting” in Social Security. Vesting means gaining an irrevocable and individual right. Social Security participants become eligible for disability and retirement benefits after they accumulate enough quarters of covered employment, but these benefits never really belong to the individuals in question; the benefits can be changed at any time, by legislation.

Worse yet, while pension plans like STRS are at least nominally funded (money is accumulated to offset the cost of future benefits), Social Security operates on a pay-as-you-go basis (current Social Security taxes are received, current Social Security benefits are paid, the surplus is spent immediately on general government expenses, and a completely imaginary IOU is written).

The retirement benefit ceiling for Social Security is far too low to replace the earned income of an educated professional — even a teacher, whose lifetime annual average salary falls below the professional range.

I agree that public-sector pension plans like STRS lock in 50-something employees. Again, this saves the public money. On a typical salary scale, and given a typical entry age, most 50-something teachers will have reached the maximum salary step. They will see no further salary growth (other than inflationary cost of living increases, in districts where these are still given).

Where private-sector employees in their 50s can compete for performance-based pay increases and for promotions, and have the potential to maintain their salaries if they switch employers, teachers are locked in to the final salary step for years and cannot hope to maintain their salaries if they switch districts (districts limit the number of years of experience credit that can be transferred for salary placement purposes). The public gets additional years of service without providing real pay increases.

R W 11 years ago11 years ago

Your article states "but courts have ruled that the Legislature can’t increase the contribution rates of current school employees without giving them a benefit equal to the value of their increased contribution, like higher pay." When STRS added the Defined Benefit Supplement Program (cash balance program) years ago which benefits current employees and in part of the the employer and State charges, STRS never increased rates the employees, employers and the State paid. So there … Read More

Your article states “but courts have ruled that the Legislature can’t increase the contribution rates of current school employees without giving them a benefit equal to the value of their increased contribution, like higher pay.” When STRS added the Defined Benefit Supplement Program (cash balance program) years ago which benefits current employees and in part of the the employer and State charges, STRS never increased rates the employees, employers and the State paid. So there are years of collections needd to be collected from employees since they are the only ones that benefit and this program contributes to the unfunded balance of STRS

Replies

John Fensterwald 11 years ago11 years ago

You may be on to something, RW. See the last paragraph of page 19 of the report. I believe it refers to the Defined Benefit Supplement Program and provides the rationale to charge employees the 2.6 percent extra that my post mentioned.

Gary Ravani 11 years ago11 years ago

It is quite clear from the report that the DBS John refers to, currently at 2% per annum, can be reduced and/or can result in higher current member contributions. This is, of course, akin to "adjusting" the way Social Security increases could be calculated downward by redefining how the "consumer price index" is set. And so the secure retirements of the 99% are under threat so that the narrow interests of the 1% and corporations … Read More

It is quite clear from the report that the DBS John refers to, currently at 2% per annum, can be reduced and/or can result in higher current member contributions.

This is, of course, akin to “adjusting” the way Social Security increases could be calculated downward by redefining how the “consumer price index” is set. And so the secure retirements of the 99% are under threat so that the narrow interests of the 1% and corporations can be protected.

The better solution, again in the report, is to raise employer contributions which would trigger a Prop 98 increase in school funding. This would bring CA some small way towards moving out of what ED Week recently, and miserably, calculated as this state’s being 49th of the 50 states in per pupil funding for K-12 education.

I say “small way” because, as the report also makes clear, the DBS program is relatively insignificant compared to the DB program. This makes combining the state’s percentage contributions to the DB and DBS program problematic (to say the least). The keys to understanding the funding issue are the state’s continued decreasing contributions to the DB and the economic instability caused by financial market malfeasance.

Paul 11 years ago11 years ago

el, the incentive that you mention saves the public a fortune, in the context of newer policies and practices in K-12 personnel management. Teachers who leave during their first five years (most do, according to the oft-repeated figure; even if the figure is exaggerated, the fraction of "leavers" is substantial) do not vest in STRS. While they may withdraw their contributions (8% of salary), they forfeit all school district (8.25%) and state (5.2%) contributions (percentages … Read More

el, the incentive that you mention saves the public a fortune, in the context of newer policies and practices in K-12 personnel management. Teachers who leave during their first five years (most do, according to the oft-repeated figure; even if the figure is exaggerated, the fraction of “leavers” is substantial) do not vest in STRS. While they may withdraw their contributions (8% of salary), they forfeit all school district (8.25%) and state (5.2%) contributions (percentages as stated in the article; I’m wondering whether the 5.2% includes previously committed payments toward the unfunded liability; I seem to remember a lower state contribution rate).

Combined with PKS layoffs, non-reelection, and abuse of the temporary and substitute classifications, the five-year vesting window gives school districts time-limited access to cheap labor. In a year, or two, or three, those teachers are replaced with other newcomers, and are left without any employer-paid retirement contributions, let alone any Social Security credits.

On the question of allowing transfers between Social Security and STRS, this would be legally and financially difficult, as Social Security is the granddaddy of defined benefit arrangements: there is an extremely weak relationship between individual contributions and individual benefits. Social Security benefits never vest and can be changed or canceled at any time by legislation. For teachers, at least, STRS is a more reliable option.

Replies

el 11 years ago11 years ago

One of the disadvantages I see with the separate STRS system is on the other end, where you have teachers in the 50+ age range who are having health issues or are just ready for different kinds of challenges and are not enjoying teaching as they once did. For these teachers, there is already a big investment in STRS, but not enough for their retirement; there's also not time to vest properly in Social Security. … Read More

One of the disadvantages I see with the separate STRS system is on the other end, where you have teachers in the 50+ age range who are having health issues or are just ready for different kinds of challenges and are not enjoying teaching as they once did. For these teachers, there is already a big investment in STRS, but not enough for their retirement; there’s also not time to vest properly in Social Security. Perhaps they could continue to contribute to STRS if they were nearly vested instead of Social Security (of course, the rates for STRS are higher; the person would have to kick out more cash). My concern is that ends up being an artificial incentive to stay in the wrong job that doesn’t actually benefit the employer or the employee.

Navigio 11 years ago11 years ago

That's true, but I would argue the whole point of any type of compensation that needs to vest is retention. Our blunt force policies generally are not subtle enough to allow distinguishing that goal from the goal of what's best for the educational system. Note that if administrators do their jobs and maintain quality educators while removing those that are not, then those two goals can be more likely to be aligned. I … Read More

That’s true, but I would argue the whole point of any type of compensation that needs to vest is retention. Our blunt force policies generally are not subtle enough to allow distinguishing that goal from the goal of what’s best for the educational system. Note that if administrators do their jobs and maintain quality educators while removing those that are not, then those two goals can be more likely to be aligned. I think it’s always going to be difficult to try to align two different vesting systems for late-in-life employees unless we actually make that a priority.

Gary Ravani 11 years ago11 years ago

“Contributions by the State of California to the Defined Benefit Program have declined from 4.607 percent to 2.791 percent since 1998.”

Quote from the STRS website.

That’s a bit different from the 5.25 state contribution John mentions above.

To Mr. E. Dogfood above: Take care, all that foaming at the mouth will eventually gum up your keyboard.

Replies

John Fensterwald 11 years ago11 years ago

Gary: The state makes contributions to CalSTRS in two ways. One is the rate it pays to the defined benefit program, now 2.791 percent. The other is 2.5 percent to the Supplemental Benefit Maintenance Account, basically a cost of living program that keeps the pensions of CalSTRS recipients from falling below 85 percent of their original purchasing power. The two combined equal 5.29 percent, as you can see on page 12 of the report.

Gary Ravani 11 years ago11 years ago

That's an interesting way of "defining" contributions. Like a bank that pays 2% on your savings account of $30K and 3% on your checking account balance of $1K. Yikes! It's a combined 5%. The fact is, the state of CA took a "pension holiday," as did many other entities that contributed to the current funding issues of many retirement systems, state, county, and municipal. Of course it must never be denied that retirement systems, like the nation's … Read More

That’s an interesting way of “defining” contributions. Like a bank that pays 2% on your savings account of $30K and 3% on your checking account balance of $1K. Yikes! It’s a combined 5%.

The fact is, the state of CA took a “pension holiday,” as did many other entities that contributed to the current funding issues of many retirement systems, state, county, and municipal.

Of course it must never be denied that retirement systems, like the nation’s entire economy, are subject to a “manufactured crisis” created by the greedy, reckless, and unregulated behavior of the financial sector.

STRS can provide for the funding of retirements at 80% of full funding quite nicely. It can do this by having the state pay its full share and employers and employees ratchet up contributions very gradually while simultaneously taking into account the changes in investment income as the economy improves.

goodsense 11 years ago11 years ago

It would be nice to see CalSTRS consider making up for some of the potential shortfall by allowing us to choose to pay into Social Security. Also, could there be a way of restructuring STRS so that it is not considered a Social Security replacement that falls under the Social Security windfall penalty. I entered the STRS system late, so I won't have a wonderful pension, but I worked many years where I … Read More

It would be nice to see CalSTRS consider making up for some of the potential shortfall by allowing us to choose to pay into Social Security. Also, could there be a way of restructuring STRS so that it is not considered a Social Security replacement that falls under the Social Security windfall penalty. I entered the STRS system late, so I won’t have a wonderful pension, but I worked many years where I paid a lot of money into Social Security. With both a low pension and resuced Social Security, I got the short end of the stick. Please note that those of us in Community Colleges have advanced degrees (PhD’s) which on average are earned at the age of 35. If you got a job right out of the university, you would only have 30 years into the pension when you were of retirement age.

It would be a nice combination to collect your full entitlement to social security and STRS. This way a reduction could be compensated for.

Replies

goodsense 11 years ago11 years ago

Oh, sorry for not editing before I submitted the above comment. Thought it might be valuable for those who do not know about the Windfall Elimination to leave a link: http://www.ssa.gov/pubs/10045.html#a0=6

el 11 years ago11 years ago

I don’t think it helps with “saving STRS” but I think it would be good policy to figure out a way for people to roll some amount of credit from Social Security into STRS or STRS into Social Security. The STRS formula is meant to assure and encourage people to spend their entire careers as educators… and I’m not sure we want to use the pension to incentivize in that way any longer.

eatingdogfood 11 years ago11 years ago

If The Democrats Didn’t Give ” Sweetheart Deals ” To Your Public Service Union.

Goon Employees To Get Reelected; You Would Have Plenty Of Money and The.

Taxpayer would have Some Spare Change in His Pockets! Democratic Hustler

Politicians + Corrupt Union Goons = BANKRUPTCY BABY! Time To Bring.

RICO Conspiracy Charges Against The Hustler Corrupt Democrats and the.

Criminal Unions!